Gjensidige "defensive dividend stock"

Gjensidige "defensive dividend stock"

As my third write-up, I will publish a piece on the insurance company Gjensidige Forsikring, ticker symbol GJF, and listed on Euronext Oslo.

Profitability and valuation numbers for the last three quarters & five-year average

Loss ratio: 66.2%/ 68.9%

Cost ratio: 14.5%/ 14.8%

Combined ratio: 80.7% / 83.7%

LTM

ROE: 26.3% / 20.8%

P/E: 16/ 16.5 at 210 kr per share

Mcap 105.5 billion NOK at 210 kr per share

The business

Gjensidige Forsikring main business is the property & casuality business. The company has been in business for more than 200 years when it started as wholly owned by its customers. Gjensidige made a public offering in late 2010 when the Gjensidigefoundation sold shares for 11.8 billion kroner. In December 2021, the foundation still owned a majority of the company at 62.2%. Gjensidge gains a competitive advantage since most of the company is in the hands of the foundation. A majority of the dividends go back to the customers and charitable donations. The foundation has paid out dividends to the customers for 12 years in a row. In 2021 the customers received 13% of their premiums back in the form of a dividend. This makes it extra attractive to stay on as a customer instead of switching towards another insurance company.

Looking at the chart above, you can see that the company is thriving and creating great results for its shareholders. The average return on equity in the last five years is 20.8%, strongly influenced by 26.3% in the latest four quarters and 25.2% in 2019.

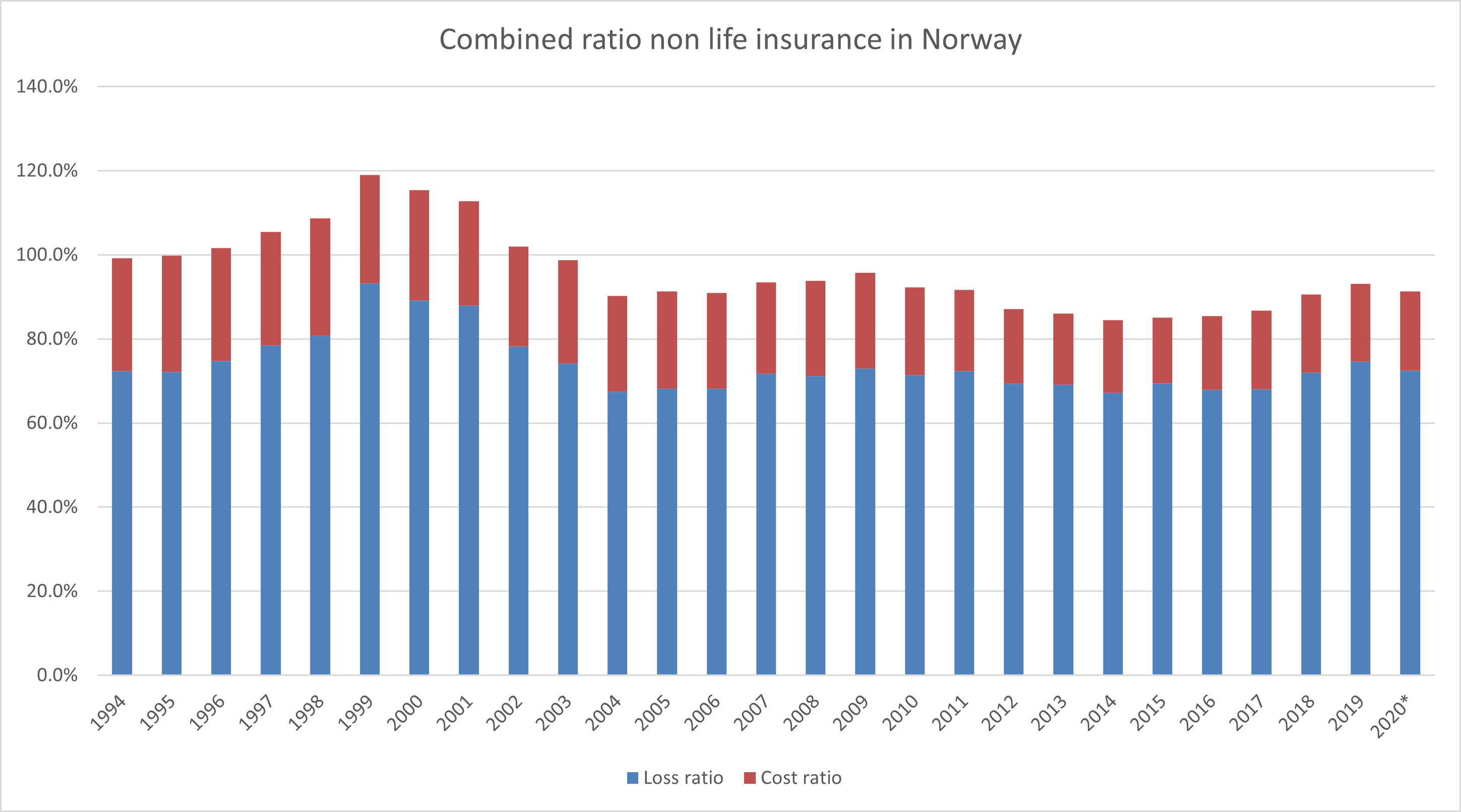

Being a non-life insurance company in Norway has been rewarding in the twenty-first century. Cost levels have steadily fallen from 26% in 1994 to under 19% in 2020. The chart below shows that the market has a high degree of consolidation, where the four largest companies have 3/4 of the market. Instead of stealing customers from competitors, the companies focus on improving operations, increasing digitalization, and reducing fraud to make the bottom line prettier.

What is driving the return on equity in the period?

Reducing the cost by implementing better IT systems is beneficial for improving efficiency. Gjensidige has been favorable output by reducing loss level from 75.5% in 2011 to 66.2% year to date. Is this trend with margin expansion set to last for another couple of years? That’s unlikely to happen since customers will probably demand to pay less for insurance if Gjensidiges margins continue to increase.

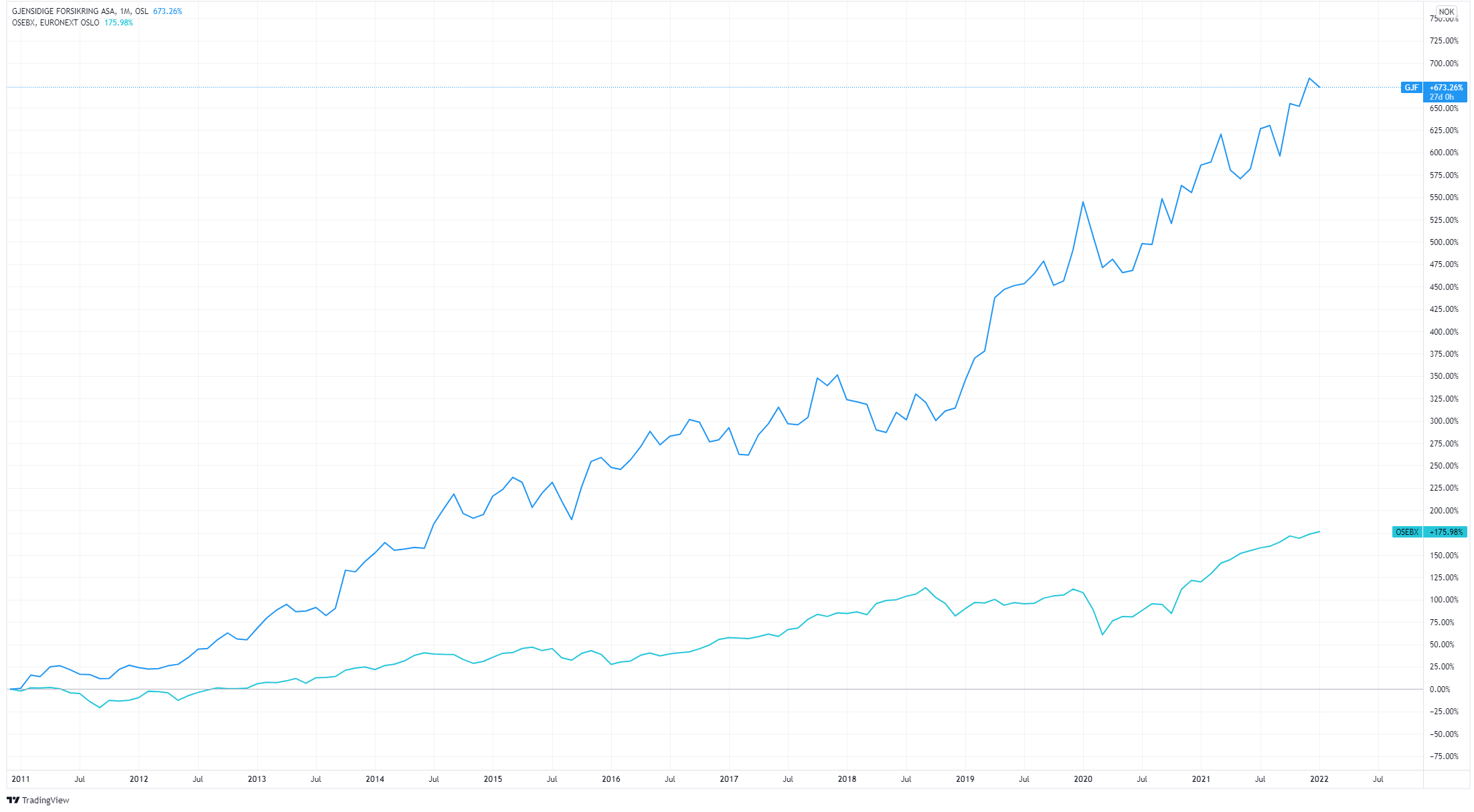

Historic return

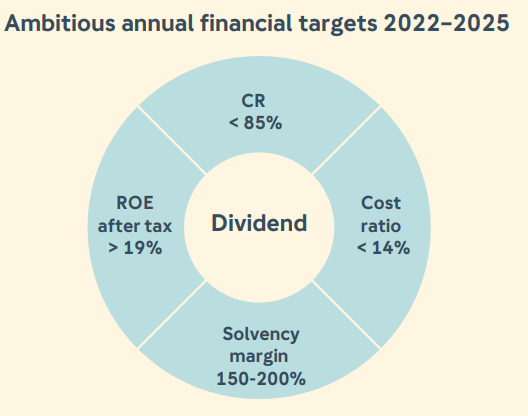

Gjensidige Forsikring has destroyed the Norwegian stock index by returning significant amounts of excess capital to shareholders, reducing costs, and delivering healthy premium growth. Large run-off gains will not last forever, but the underlying business is strong, demonstrated by the company's target for 2022-2025 communicated at the capital markets day back in November.

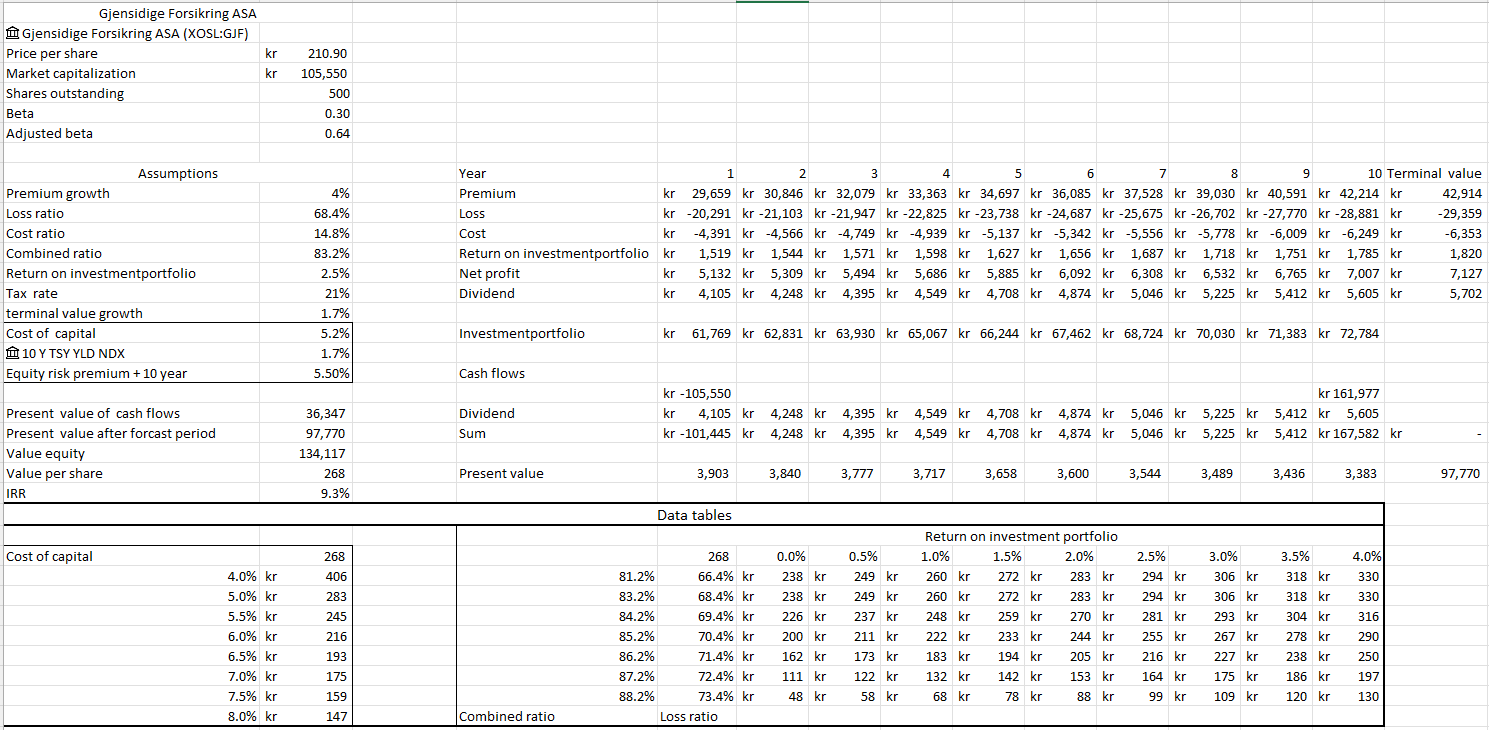

What’s the company worth

Gjensidige is obviously not the next high-growth company, but it provides high dividend income in combination that it's not a great deal of risk in the investment case. In good times it will be beaten by more cyclical stocks that run on the market's strength, but when the market sentiment takes a beating, this stock provides excellent downside protection. People will still need insurance, and their investment portfolio consists of primarily low-risk assets.

In my analysis, I used conservative numbers, but one can argue that the discount rate is too low even though the company's beta suggests that the company has low systemic risk. Instead of using the company's beta, I used the beta of the property & causality industry in the US. The market risk premium has been approximately between 5-6% for a while, and that's why I use 5.5% in my analysis.

In my view, the company gives a decent risk/reward with a potential 9% annual return at these levels. The low-risk profile gives it a fair value of 271 kr per share with upside potential if they’re able to decrease cost levels with increased digitization. If you have different views with cost and loss levels, return on the investment portfolio, or cost of capital, you can look at the data table and see how other estimates change the fair value estimate.

I’m not a bank & insurance analyst, but I do these kinds of valuation exercises to let me know If I can buy a great company at a reasonable price. In my opinion Gjensidige Forsikring fits my criterias. Remember building a model or analysis that’s too complicated doesn’t necessarily make your chances of being right any better than trying to see if the numbers make sense.

If you would like to download the excel file you can click on this link and become a subscriber at the same time!

Disclaimer

Always do your own research before investing! I hope that you enjoyed this post but it should not be considered an encouragement to buy the companies that I include in my portfolio or be taken as financial advice. If you want to receive investment advice you should contact a professional.

Sources:

https://www.gjensidige.no/group/investor-relations

https://www.finansnorge.no/statistikk/skadeforsikring/markedsandeler/

https://www.finansnorge.no/en/statistics2/non-life-insurance/

https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/Betas.html